Q2 FY18 Results Update and Frequently Asked Questions

Q1. What is ITC's Vision and Mission?

Answer:

Vision:

Sustain ITC's position as one of India's most valuable and admired corporations through world-class performance, creating growing value for the Indian economy and the Company's stakeholders.

Mission:

To enhance the wealth generating capability of the enterprise in a globalising environment, delivering superior and sustainable stakeholder value.

Q2. How does the Company effectively manage a highly diversified business portfolio? What is the Company's Corporate Governance structure?

Answer: ITC's 'Strategy of Organisation' is crafted in a manner that enables focus on each business while harnessing the diversity of the portfolio to create unique sources of competitive advantage. Please refer to the following link http://www.itcportal.com/about-itc/values/corporate-governance-structure.aspx for details of ITC's 3-tier Governance Structure.

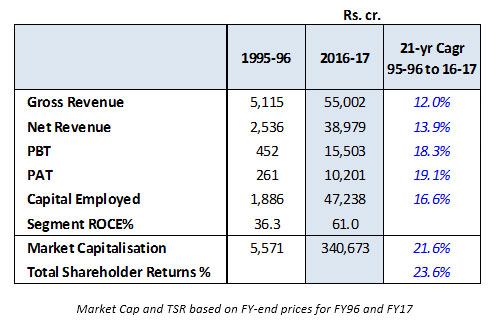

Q3. What is the Company's shareholder value creation track record?

Answer: ITC has been a consistent performer in terms of shareholder value creation. During the period 1995/96 to 2016/17, Total Shareholder Returns have clocked compound annual growth rate of 23.6% significantly outperforming the Sensex (10.9%).

Q4. (a). Why has reported Gross Revenue from sale of products and services declined by 28% in Q2 FY18 as compared to Q2 FY17?

Answer: Consequent to the introduction of Goods and Services Tax (GST) with effect from 1st July 2017, Central Excise [other than National Calamity Contingent Duty (NCCD) on cigarettes], Value Added Tax (VAT) etc. have been replaced by GST. In accordance with Indian Accounting Standard - 18 on Revenue and Schedule III of the Companies Act, 2013, GST, GST Compensation Cess, VAT, etc. are not included in Gross Revenue from sale of products and services for applicable periods. In view of the aforesaid restructuring of indirect taxes, Gross Revenue from sale of products and services and Excise duty for the quarter and six months ended 30th September, 2017 are not comparable with the previous periods.

Q4. (b). What is the growth in Revenue for the quarter on a comparable basis?

Answer: On a comparable basis, Gross Sales Value (net of rebates/discounts) stood at Rs. 16391.58 crores representing a growth of 3.9%. Gross Sales Value includes GST, GST Compensation Cess, Service Tax, VAT, Luxury Tax etc., as applicable for the reported periods.

Q5. Please provide a brief overview of Q2 FY18 results.

Answer: The Company's performance during the quarter was relatively subdued due to severe pressure on the legal Cigarette industry and sluggish demand conditions prevailing in the FMCG industry. Operating conditions in the Agri Business and Hotels segment also remained challenging. Gross Sales Value (net of rebates/discounts) stood at Rs. 16391.58 crores representing a growth of 3.9%. Profit Before Tax at Rs. 3944.29 crores and Net Profit at Rs. 2639.84 crores registered a growth of 3.1% and 5.6% respectively during the quarter. Over 85% of the incremental value-added by the Company during the quarter accrued to the Exchequer. Earnings Per Share for the quarter stood at Rs. 2.17 (Q2 FY '17: Rs. 2.07) Total Comprehensive Income (TCI) for the quarter stood at Rs. 2610.80 crores representing a growth of 5.5%.

Q6. (a). Why has 'Consumption of Raw Material etc. (net)' increased by Rs. 685 crores during Q2FY18 as compared to Q2 FY17?

Answer: Consumption of Raw Material etc. (net) includes Excise Duty on changes on Inventory. Excluding the same, the comparable growth is 0.3%.

Q6. (b). Why has 'Other Expenditure'declined by Rs. 169 crores from Rs. 1759 crores in Q2 FY17 to Rs. 1590 crores in Q2 FY18?

Answer: Other Expenditure for Q2 FY18 is lower by 10% Vs. Q2 FY17 mainly due to lower Rates & Taxes, repairs and maintenance, contract processing charges and consumption of stores and spare parts partly offset by higher write-off and provision for doubtful debts.

Q7. What is the rationale for the Company's investments in the FMCG space?

Answer: ITC's entry into a wider range of FMCG products in recent years is in line with its strategy of creating multiple drivers of growth. The Indian FMCG industry is expected to grow rapidly driven by increasing affluence, urbanisation and a young workforce on the one hand and relatively low levels of penetration and per capita usage on the other. The Company seeks to participate in the exciting growth prospects of the FMCG industry by leveraging its institutional strengths namely, deep consumer insight, proven brand building capability, manufacturing excellence, deep and wide distribution network, packaging and printing knowhow, agri-commodity sourcing expertise and cuisine knowledge.

Q8. Please provide an overview of the Company's progress in the new FMCG businesses. What is the Company's goal in the new FMCG businesses?

Answer: The FMCG industry witnessed further deceleration in growth rate during 2016/17 with demand conditions remaining subdued for the fourth successive year. The much anticipated pick-up in consumption expenditure on the back of good monsoons in 2016, low inflation and implementation of the recommendations of the 7th Pay Commission did not play out fully. The incipient recovery in demand witnessed during the middle of the year was adversely impacted by the cash crunch especially during the third quarter. Further, the industry had to contend with sharp escalation in the cost of major commodities in the midst of heightened competitive intensity, leading to compression in margins.

The Company's FMCG-Others Segment Revenue growth in 2016-17 was relatively subdued due to reasons as aforestated. While most categories recovered progressively after severe disruption in operations in the initial period of the cash crunch, the impact on the Lifestyle Retailing and Education & Stationery Products Businesses was more amplified and prolonged. This, inter alia, led to heavy discounting, advancement of 'end of season sales' and rebalancing of inventory pipelines by trade in these Businesses. Consequently, Segment Revenue at Rs. 10511.83 crores grew by 8.0% over the previous year. Segment Results also reflect the impact of sustained investment in brand building and gestation costs of new categories viz., Juices, Dairy, Chocolates and Coffee, sharp increase in input cost (particularly of Wheat, Maida, Sugar, Cashew, Soap Noodles) besides deceleration in sales momentum due to the cash crunch.

The Company continued to make investments during the year towards enhancing brand salience and consumer connect while simultaneously implementing strategic cost management measures across the value chain. Several initiatives were also implemented during the year towards leveraging the rapidly growing e-commerce channel with a view to enhancing the reach of the Company's products and harnessing digital and social media platforms for deeper consumer engagement.

In 2016-17, three Company-owned units were commissioned to cater to the requirements of the Branded Packaged Foods and Personal Care Products Businesses. Significant progress was also made during the year in constructing several state-of-the-art owned Integrated Consumer Goods Manufacturing and Logistics facilities across regions to secure capacity and enable the FMCG-Others Businesses to rapidly scale up in line with long-term demand forecast. Currently, over 20 projects are underway and in various stages of development - from land acquisition/site development to construction of buildings and other infrastructure.

The FMCG Businesses comprising Branded Packaged Foods, Personal Care Products, Education and Stationery Products, Lifestyle Retailing, Incense Sticks (Agarbattis) and Safety Matches have grown at an impressive pace over the past several years. Today, the Company's vibrant portfolio of brands represents an annual consumer spend of nearly Rs. 14000 crores in aggregate. These brands have been built organically by the Company over a relatively short period of time - a feat unparalleled in the Indian FMCG industry. In terms of annual consumer spend, Aashirvaad and Sunfeast are today over Rs. 3500 crores and Rs. 3000 crores respectively; Classmate, YiPPee! & Bingo! are over Rs. 1000 crores each and Vivel, Mangaldeep & Candyman are over Rs. 500 crores each. These world-class Indian brands support the competitiveness of domestic value chains of which they are a part, ensuring creation and retention of value within the country.

The Company's FMCG brands have achieved impressive market standing in a relatively short span of time. Today, Aashirvaad is No. 1 in Branded Atta, Classmate is No. 1 in Notebooks, Sunfeast is No. 1 in the Cream Biscuits segment, YiPPee! is No. 2 in Noodles, Bingo! is No. 2 in Snack foods, Engage is No. 2 in Deodorants and Mangaldeep is No. 2 in Agarbattis.

The Indian FMCG market is at an inflection point and the Company continues to remain extremely agile and responsive to the emerging trends shaping the future of the industry. Some of the noteworthy consumer trends include the emergence of health and wellness products as a key consumer need; increasing preference for products rooted to 'Indianness' and with regional/cultural connects; rising importance of high quality, hygienic and environmentally sustainable products; increasing need for customised products and bespoke experiences; growth in demand for 'on-the-go' consumption formats and rising influence of social media and digitalisation on consumer preferences and shopping behaviour. Similarly, the FMCG market construct is likely to undergo rapid change driven by exponential growth in middle and rural India and the emergence of relatively new channels such as Modern Trade and e-commerce.

The Company seeks to rapidly scale up the FMCG Businesses leveraging its institutional strengths viz. deep consumer insight, proven brand building capability, a deep and wide distribution network, strong rural linkages and agri-commodity sourcing expertise, packaging know-how and cuisine knowledge. In addition, the Company continues to make significant investments in Research & Development and focus on consumer insight discovery to develop and launch disruptive and breakthrough products in the market place.

Q9. Please provide a revenue split of the FMCG-Others Segment.

Answer: The Branded Packaged Foods Businesses represent the largest component of this segment, accounting for ~76% of Segment Revenue. The Personal Care Business and Education and Stationery Products Business account for ~8% and ~7% each of Segment Revenues respectively.

Q10. What are the new FMCG categories that the Company is likely to enter over the short to medium term?

Answer: With aspirations to become the No.1 FMCG player in India, the Company continuously evaluates opportunities to grow in the FMCG space. While it is anticipated that the FMCG industry will take a few more quarters for demand revival, the green shoots of economic recovery, expectations of normal monsoons, low inflation, partial implementation of the recommendations of the 7th Pay Commission and the 'One Rank One Pension' scheme augur well for the industry. The structural drivers of long-term growth such as increasing affluence and consumer awareness, a young and expanding workforce and increasing urbanisation amongst others, remain firmly in place and the FMCG industry is poised for rapid growth in the ensuing years.

The choice of category is guided by its growth prospects, profitability profile and the ability of the Company to effectively leverage its institutional strengths with a view to achieving leadership status within a reasonable time frame. Synergies with existing categories in terms of overlap of distribution reach, brand extension possibility, procurement efficiencies etc. are considered while choosing new categories.

Chocolates, Dairy, Tea & Coffee, processed, frozen foods and fresh fruits & vegetables are some of the interest areas in this context.

Q11. What is the margin profile of the Branded Packaged Foods Business?

Answer: The Branded Packaged Foods Businesses of the Company comprise 'Confections', 'Staples, Snacks and Meals' and 'Dairy & Beverages'. These Businesses have evolved over a period of time and are currently at different stages of their lifecycles. As such, the revenue dimensions, cost structures and profitability profiles of each of these businesses are distinct from the other. For example, EBIT margin is in the high single digit range for the Staples business (first full year of launch: 2002/03) while the same is in the low single digit range for the Snack Foods business (first full year of launch: 2007/08) representing upfront investments towards category development and brand building.

Overall, the mandate for each category is to achieve best-in-class margins within a reasonable period of time.

Q12. What is the margin profile of the Personal Care Products Business? When will it break-even?

Answer: The Personal Care Products Business presently comprises the 'Personal Wash', 'Fragrancing Products', 'Skin Care' and 'Antiseptic Liquid' categories. The Company continues to make significant investments in this Business primarily in the area of brand building, R&D and product development towards competing effectively with incumbent players comprising firmly entrenched MNCs and domestic companies.

Presently, each category is operating at industry benchmarked gross margins. With enhanced scale and consumer connect, each category is expected to earn best-in-class EBIT margins progressively over the medium-term.

Q13. What are the Company's targets in the FMCG-Others space? What does the Company envision in terms of revenue and profits in this segment, over the medium and long-term?

Answer: ITC's endeavour is to become the No.1 FMCG player in India driven by the existing portfolio as well as entry into new categories. In this regard, the Company is aiming for revenue of Rs. 100,000 crores from the new FMCG businesses by the year 2030.

Over the medium term, the Company seeks to grow revenues of each category within the FMCG-Others segment at a rate which is well ahead of industry. With enhanced scale and consumer connect, each category is expected to earn best-in-class EBIT margins, progressively over the medium-term.

Q14. Would ITC contemplate acquisitions in order to achieve its vision in the Other FMCG segment?

Answer: ITC examines prospects for inorganic growth that arise from time to time not only in this business segment but also in the other businesses. The Company continues to evaluate opportunities to grow its businesses through Acquisitions and Joint Ventures and is guided by considerations such as strategic fit, valuation, financial viability, ease of integration etc.

The Company's 'Savlon' and 'Shower to Shower' brands, acquired earlier, have been leveraged to strengthen its position in the personal care space by expanding its existing product portfolio and gaining access to newer consumer segments and markets. The offerings have garnered significant consumer franchise and are well poised for rapid growth.

The Company's 'B Natural' brand, acquired earlier, was leveraged to foray into the fast growing Juices category. B Natural range of juices, currently available in many exciting variants, has garnered impressive consumer traction in a relatively short span of time and is well poised for rapid growth.

The Company's recently acquired 'Charmis' brand has been leveraged to launch moisturising skin cream during Q2 FY18.

Q15. Please provide an update on the Company's progress in the FMCG-Others Segment during the quarter.

Answer: Segment Revenue registered robust growth of 10% on a comparable basis despite muted demand environment and disruption due to GST transition. Such growth was driven by strong performance of the Branded Packaged Foods and Personal Care Businesses partly offset by the impact of ongoing restructuring of retail & trade footprint in the Lifestyle Retailing Business. While offtake in the retail channel has normalised progressively through the quarter, the wholesale channel is yet to fully recover. Market standing stood enhanced across major categories, particularly in atta, potato chips, premium cream biscuits and deodorants.

The Branded Packaged Foods Businesses posted healthy growth in revenue led by atta, snacks and noodles.

- In the Staples, Snacks and Meals Business, 'Aashirvaad' atta continued to perform well consolidating its leadership position across markets.

The 'Bingo!' range of snack foods recorded robust growth driven by 'Yumitos' potato chips and 'Tedhe Medhe'. Several innovative products such as Tedhe Medhe 'Lime' & 'Tomato Masti' and Mad Angles 'Kasundi', tailored to suit regional tastes and preferences were launched during the quarter. The Business also introduced Bingo! 'No Rulz' - a-first-of-its-kind offer comprising 4 different shapes of the product in a single pack. The product is available in 3 exciting flavours and has received encouraging response from consumers.

In the Instant Noodles category, YiPPee! continued to perform well leveraging its superior value proposition anchored on best-in-class product quality and taste. The recently launched YiPPee! Mood Masala variant continued to garner increasing consumer franchise across target markets. - In the Confections Business, 'Sunfeast' biscuits performed well with 'Dark Fantasy Choco Fills', 'Sunfeast Marie' and 'Mom's Magic' continuing to enhance market standing. During the quarter, the Business launched 'Dark Fantasy Creations' - a campaign themed around 'making exquisite desserts with Dark Fantasy' in collaboration with ITC Hotels. Product portfolio was augmented with the introduction of innovative products anchored on the health vector in select markets viz. 'Farmlite Active Protein Power' - a unique offering that combines the goodness of roasted Bengal Gram flour with great taste, 'Farmlite Digestive High Fibre' biscuits with the goodness of five grains and 'Sunfeast A2 Naat Maad Paal' biscuits enriched with native Indian cow milk. Portfolio premiumisation continued in the Confectionery category with the share of 'Re.1 and above' products further increasing during the quarter. The Business launched 'Candyman Cola Josh' - an innovative offering with a 'fizzy' powder at the heart of the candy that provides a sensorial experience akin to a soft drink.

- In the Dairy and Beverages Business, B Natural juices continued to register strong growth leveraging a portfolio of differentiated products including a wide range of 'Not from Concentrate' variants that are made directly from fruit pulp thereby providing consumers a more nutritive and natural tasting experience. The recently launched, first-to-market '100% Not from Concentrate Pomegranate juice' continued to garner impressive consumer franchise in the health and wellness segment. A range of gift packs launched during the quarter ahead of the festive season was well received in the target segments. In Dairy, 'Aashirvaad Svasti' ghee was extended to the Delhi & NCR markets during the quarter.

During the quarter, the Business expanded the footprint of 'Fabelle Chocolate Boutiques', hitherto available exclusively across ITC Hotels, to premium outlets in Bengaluru, Kolkata and Chennai. The Fabelle range of exquisitely crafted luxury gift packs with interesting personalisation options received encouraging response from discerning consumers in the festive gifting season.

The Personal Care Products Business continues to focus on product mix enrichment and augmenting its product portfolio. The 'Engage On' range of pocket perfumes recorded robust growth on the back of its unique value proposition combining convenience and affordability. The Engage portfolio stood expanded during the quarter with the launch of 'Engage On+' premium perfumes for women. The Fiama shower gel range and the recently launched Vivel Lotus Oil soap continue to garner impressive traction with consumers. During the quarter, the Business also launched moisturising skin cream under the recently acquired 'Charmis' brand.

The Business continued to leverage innovative brand campaigns and social media platforms to deepen consumer engagement. In line with its brand credo - 'Ab Samjhauta Nahin', Vivel teamed up with Ms. Srishti Bakshi, the 'UN Women Empower Champion for Change 2017', in her journey to raise awareness on safety for women and women's rights.

The Company made steady progress during the quarter towards setting up state-of-the-art owned integrated consumer goods manufacturing facilities at Panchla (West Bengal) and Kapurthala (Punjab). These facilities are expected to commence operations in phases, beginning the ensuing quarter. Currently, over 20 projects are underway and in various stages of development - from land acquisition/site development to construction of buildings and other infrastructure.

Please refer to the FMCG - Others section in the Report of the Directors & Management Discussion and Analysis for the financial year ended 31st March 2017 and Media Releases on quarterly results for further details.

Q16. Please provide an update on the Cigarettes business.

Answer: Pressure on the legal cigarette industry escalated significantly during the quarter on account of the steep increase in tax incidence under the GST regime and additional burden on the Business due to GST transition costs. The legal cigarette industry, already reeling under the cumulative impact of steep increase in taxation over the last 5 years and intense regulatory pressures, was further impacted by the sharp upward revision in GST Compensation Cess announced by the GST Council at its meeting on 17th July, 2017.

While the intention of the Government was to correct an apparent anomaly in cigarette taxation under the new tax regime announced earlier on account of the removal of the cascading effect of Excise Duty which existed in the pre GST regime, the upward revision resulted in significantly higher tax incidence on cigarettes compared to the pre GST scenario which is not in keeping with the fundamental principle of revenue neutrality. In fact, the combined impact of increase in Excise Duty announced by the Union Budget 2017 and the revision in GST Compensation Cess as aforestated resulted in an incremental tax burden of over 20% on the Company. It is pertinent to note that the cumulative growth in tax incidence on cigarettes, after cognising for the latest increase in Cess rates, stands at a staggering 202% since 2011-12, i.e. the last 6 years.

Further, the Cigarette Business had to contend with additional costs associated with the transition to GST due to non-availability of Additional Duty Surcharge credit on transition stocks and the unanticipated revision of GST Compensation Cess w.e.f. 18th July 2017 which impacted pipeline stocks.

It is apprehended that the sharp increase in tax incidence on cigarettes will further increase the huge tax arbitrage available to unscrupulous players and provide a fillip to smuggling syndicates. This will severely undermine the legal cigarette industry and adversely impact tobacco farmers and the revenue objective of the Government. According to an independent study conducted by Euromonitor International, India is today the 4th largest market for illegal cigarettes in the world. It is estimated that almost 68% of the tobacco consumed in the country remains outside the tax net on account of evasion . The proliferation of these tax-evaded products has resulted in significant losses to the Exchequer, in excess of Rs. 9000 crores per annum according to an independent study conducted by the Federation of Indian Chambers of Commerce and Industry (FICCI).

As reported earlier, the significant decline in legal cigarette volumes and the consequent reduction in the utilisation of Indian Flue-cured Virginia (FCV) tobacco has adversely impacted the livelihoods of over 45 million tobacco farmers, farm workers and others dependent on the tobacco sector. Besides, the soft demand for Indian FCV tobacco has prompted consecutive reductions in the authorised tobacco crop size in 2015-16 and 2016-17. This, in turn, has also led to lower exports of tobacco. In fact, since 2013-14, the annual earnings of tobacco farming community has shrunk by more than Rs. 1,500 crores due to drop in offtake of tobacco for the manufacture of domestic legal cigarettes.

Although legal cigarettes account for only about 11% of total tobacco consumption in the country, they contribute more than 87% of tax revenue from the tobacco sector. The other types of tobacco products contribute barely 13% of tax revenue from the tobacco sector despite accounting for 89% of total tobacco consumption.

Unfortunately, the taxation policy of the country is largely cigarette-centric and based on western models of tobacco taxation. This policy is not suitable for India since duty-paid cigarettes account for only about 11% of tobacco consumption in the country as compared to the global average of more than 90%. The Company continues to engage with policy makers for a tobacco taxation policy that is non-discriminatory, helps combat the problem of illegal cigarettes and addresses the issues of all stakeholders, particularly the tobacco farmers, the Exchequer and consumers. Such a policy will not only help maximisation of the revenue potential of tobacco even in a shrinking basket of tobacco consumption but also address the tobacco control and health objectives of the Government.

Despite the extremely challenging operating environment, the Company sustained its leadership position in the industry through relentless focus on delivering world-class products, continuous innovation & value addition and best-in-class execution.

Please refer to the FMCG - Cigarettes section in the Report of the Directors & Management Discussion and Analysis for the financial year ended 31st March 2017 and Media Releases on quarterly results for further details.

Q17. Is the pressure on volumes similar across the different segments i.e. King Size filters, Longs, Regular filters and filter cigarettes of 'length not exceeding 65 mm'?

Answer: While all segments are witnessing pressure on volumes, the sub 65 mm segment is relatively less impacted.

Q18. What is the Company's view on cigarette volume trends over the medium to long term?

Answer: As aforestated, the cumulative growth in tax incidence on cigarettes, after cognising for the latest increase in Cess rates, stands at a staggering 202% since 2011-12, i.e. the last 6 years. The additional tax burden caused by the increase in the Compensation Cess rates, as aforestated, will exacerbate the pressure on the entire legal cigarette value chain in the country. The legal cigarette industry is already reeling under a huge tax burden on account of the continuous increase in Excise Duties on cigarettes which has resulted in a 25% decline in legal cigarette industry volumes since 2012/13.

As highlighted earlier, the share of legal cigarettes in overall tobacco consumption is 11% in India. While this indicates room for growth in legal cigarette volumes going forward, this would largely depend on the taxation and regulatory policy on cigarettes adopted by the Government. Such growth potential was demonstrated during the period 2004/05 to 2006/07 and again, more recently, in 2009/10 and 2011/12 - years in which taxes / duties growth were moderate.

A stable, fair and equitable India-centric cigarette taxation and regulatory policy which recognises the unique tobacco consumption pattern in the country is critical to realising the full economic potential of the tobacco sector in India.

The Company continues to engage with the concerned authorities, both at the Central Government and State level, in this regard.

Q19. At what rate are Cigarettes taxed under the GST regime? What is the impact of GST on Cigarettes Business?

Answer: Cigarettes are exigible to tax under the GST regime at the peak rate of 28%. Additionally, a GST Compensation Cess which includes an Ad Valorem component and a Specific Tax component based on cigarette length, has also been imposed. The National Calamity Contingent Duty (NCCD) component of Excise Duty continues to be levied as earlier based on the length of the cigarette.

Please see response to question no. 16 for impact of GST on Cigarette Business.

Q20. What is the status on introduction of larger graphic health warnings on packs?

Answer: The legal cigarette industry in India continues to grapple with an increasingly stringent regulatory framework. As reported last year, the proposal for increasing the size of the Graphic Health Warnings (GHW) from 40% of the surface area on one side of the cigarette package to 85% of the surface area of both sides of the cigarette package with effect from 1st April 2015 was kept in abeyance pending the recommendations of the Parliamentary Committee on Subordinate Legislation (PCOSL), which had been entrusted with the responsibility of examining the issues consequent to introduction of a larger GHW. However, even before the PCOSL submitted their final report on the matter, the larger health warnings were notified for implementation with effect from 1st April 2016. In the interim, on 15th March, 2016 the PCOSL, in its final report recommended that the size of the GHW should be restricted to 50% on both sides of the cigarette package and not 85% as proposed by the Government. Pursuant to the order of the Honourable Supreme Court, the Honourable High Court of Karnataka has heard the Company's and other writ petitions challenging the revised GHW and has reserved its judgement.

Q21. What would be the likely impact of the larger graphic health warnings on packs on the cigarette industry?

Answer: The 85% GHW is excessively large, extremely gruesome and unreasonable. There is no evidence that cigarette smoking would cause the diseases depicted in the pictures or that large GHW will lead to reduction in consumption. As reported last year, this inadequacy of evidence prompted an appeals court in USA to hold the US FDA's proposal for introduction of similar GHW in that country as unconstitutional. It is pertinent to note that the global average size of GHW is only about 30% coverage of the principal display area. Further, over 100 countries representing 60% of the signatories to the Framework Convention on Tobacco Control (FCTC) have not adopted GHW. In fact, the three countries that account for about 51% of the world's cigarette consumption viz. USA, Japan and China, have not adopted pictorial / graphic warnings and have prescribed only text-based warnings on cigarette packages. Moreover, several major tobacco producing countries, including the USA, are either not parties to the FCTC or are very recent signatories. These countries have taken into consideration the interests of their tobacco farmers in deciding whether or not to adopt large or excessive pictorial warnings.

The excessively large GHWs prevent consumers from making an informed choice in a competitive market, since they are denied adequate information about the brand on the cigarette packages. The Company believes that such GHW also devalues the Intellectual Property Rights of brand owners and sub-optimises the large investments made over the years in creating and nurturing the brands. Additionally, studies by independent market research agencies show that consumers tend to prefer the smuggled brands of international cigarettes which do not carry the GHWs mandated by Indian Laws. The absence of GHWs on packages of such contraband cigarettes makes consumers perceive them to be a "safer alternative" notwithstanding the fact that the origins and age of such contraband stocks are not determinable. The absence of GHWs along with the significantly lower cost of these contraband cigarettes, due to reasons of tax evasion, only serve to accelerate the growth of the illegal cigarette segment.

The unintended consequences of the extant tobacco taxation and regulatory framework may be summarised as follows:

- Progressive decline in legal cigarette volumes in favour of lightly taxed and tax-evaded tobacco products resulting in sub-optimisation of the revenue potential of the tobacco sector and significant loss to the Exchequer.

- About 68% of the tobacco consumption in the country remaining outside the tax net.

- Availability of illegal cigarettes and other tobacco products of dubious quality and hygiene to consumers at extremely affordable prices.

- Adverse impact on the livelihood of tobacco farmers and others dependent on tobacco for their livelihood.

- Fillip to the growth of illegal cigarettes in the absence of statutory GHW on smuggled international brands.

The Company continues to represent to the Government for the implementation of an equitable, evidence based and pragmatic tobacco taxation and regulatory framework that cognises for the economic imperatives of the country whilst, simultaneously, supporting the tobacco control objectives of the Government.

Q22. What are the Company's plans in the 'other tobacco and nicotine products' space?

Answer: In recognition of the growing trend of consumers seeking alternative sources of nicotine like Electronic Vaping Devices (EVD), the Company expanded its EON brand of EVDs to several new markets in 2016-17. The rechargeable variant, 'EON Charge', launched in the previous year was extended to several new markets and a disposable variant, 'EON ZIP', was launched during the year. Initial consumer response to this variant has been positive. The market for this category is, however, at an embryonic stage globally and, as reported last year, the regulatory oversight is still evolving. Accordingly, the Company remains engaged with policy makers for an apposite regulatory framework for this emerging category.

In the Nicotine Gum category, the Business extended the KwikNic brand to several new markets and has received encouraging response from consumers.

Q23. Please provide an update on the Company's Hotels business.

Answer: During the quarter, Room revenue grew at a healthy pace on account of increase in ARRs. However, Food & Beverage revenue growth was impacted by highway liquor ban which prevailed for a significant part of the quarter. While Segment Results improved as compared to the corresponding quarter in the previous year, the same remained muted due to the challenging business context as aforestated and gestation costs of the recently commissioned ITC Grand Bharat, Gurgaon. Renovation work at ITC Maurya and ITC Maratha also weighed on overall performance. The Business commissioned WelcomHotel Coimbatore on 1st October '17

The Company's Hotels business remains amongst the fastest growing Indian hospitality chains with around 100 properties across the country under four distinct brands - 'ITC Hotel' in the Luxury segment, 'WelcomHotel' in the Upper-Upscale segment, 'Fortune' in the Mid-market to Upscale space and 'WelcomHeritage' in the Leisure & Heritage segment. The Business continues to focus on strengthening the equity and differentiation of the ITC Hotels brand anchored on unique and path-breaking 'Responsible Luxury' initiatives, culinary excellence and personalisation of guest services. The Business also extended several 'Responsible Luxury' themed culinary initiatives and promotions under the 'Kitchens of India' banner.

'Club ITC', the Company's pan-ITC consumer loyalty programme with a current membership base of around 3.5 lakh premium consumers, continues to gain franchise amongst the premium clientele of ITC Hotels and Lifestyle Retailing Businesses. In 2016-17, the Business entered into a strategic partnership for integration of Club ITC with Starwood Preferred Guest (SPG), global loyalty programme of Starwood, enabling members to redeem points at over 1200 hotels worldwide. The 'Club ITC Culinaire' dining loyalty programme is also gaining popularity.

The Company's Hotels Business continues to receive accolades for its world-class properties and service excellence. ITC Grand Bharat was recognised as #1 amongst the 'Top Resorts in Asia' on the coveted Conde Nast Traveler U.S. Readers' Choice Awards for the second consecutive year, while ITC Grand Chola was the winner in the 'Sustainable Operations' category at the HICAP Sustainable Awards.

The Food & Beverage segment continues to be a major strength of the Company with some of the most iconic brands in the country. The iconic 'Bukhara' restaurant at the ITC Maurya, New Delhi continues to receive international recognition and remains a favourite in India. Bukhara was recently ranked amongst the 'Greatest Restaurants around the Globe' by Conde Nast Traveler U.S., in addition to being recognised as a 'Legendary Restaurant' at the Times Food Awards. 'Ottimo', 'EDO', 'Tian' and 'Pan Asian' continued to win accolades at the Times Food Awards. The Company's internationally acclaimed spa brand, 'Kaya Kalp', won several accolades at the Asia Spa Awards - while the spa at ITC Grand Bharat was adjudged the 'Best Spa' in the Resort category, the one at ITC Mughal received the 'Hall of Fame' award.

The Company's Hotels Business continuously strives to reduce water and energy consumption and enhance the usage of renewable energy to meet its overall energy requirements. Such commitment to the Triple Bottom Line is manifest in the Business's 'Responsible Luxury' ethos and has enabled it to position itself as the greenest luxury hotel chain in the world. It is pertinent to note that over 50% of the total electrical energy consumption of the Business is currently met through renewable sources.

The Company remains committed to building world-class hotel properties in view of the long-term potential of the Indian hospitality sector. The Business made steady progress in the construction of luxury hotels at Hyderabad, Kolkata and Ahmedabad. In addition, the Company's wholly-owned subsidiary in Sri Lanka made good progress towards setting up a luxury hotel christened 'ITC One' and a super-premium residential apartment complex, 'Colombo One - Private Residences', situated at a strategic location in Colombo. Excavation and allied works have been completed and the main construction activity is underway.

The Business is progressing growth plans towards enhancing its presence in the Upper-Upscale segment under the WelcomHotel brand. WelcomHotel Coimbatore, a 103 key property, was commissioned on 1st October '17 in the heart of the textile hub of India. Construction of WelcomHotels at Guntur and Bhubaneswar is making steady progress. As reported earlier, the Company has entered into a management contract with 'WelcomHotel Kences Palm Beach' Mamallapuram. With this, nearly a 1000 rooms are under management contract and plans are on the anvil to expand presence through this route.

The 'Fortune' brand strengthened its leadership position and expanded its presence with the addition of two new hotels during the year. The number of operational hotels under the Fortune brand presently stands at 46 across 34 cities. The 'WelcomHeritage' brand remains the country's most successful and largest chain of heritage hotels with 35 operational hotels.

The Company's Hotels Business, with its world-class properties, globally benchmarked levels of service excellence and customer centricity, is well positioned to sustain its leadership status in the industry.

Please refer to the Hotels section in the Report of the Directors & Management Discussion and Analysis for the financial year ended 31st March 2017 and Media Releases on quarterly results for further details.

Q24. Please provide an update on the Company's Agri Business.

Answer: The performance of the Agri Business Segment during the quarter was impacted by shortage of leaf tobacco in Andhra Pradesh due to lower crop output on account of drought in 2016 & adverse crop quality, relative strength of the Indian Rupee vis-á-vis currencies of competing origins and limited trading opportunities in other agri-commodities.

Global production of Flue Cured Virginia (FCV) tobacco registered a decline of 8.5% in 2016, with crop output in Brazil degrowing by nearly 20%. Indian FCV crop production declined for the second successive year, dropping by nearly 20% during 2016 to 217 million Kgs., mainly due to lower Andhra crop consequent to the Tobacco Board's decision to reduce the authorised crop size by 50 million Kgs. over 2015. Consequently, FCV farm prices recorded a sharp increase in 2016-17.

Whilst the reduction in global FCV output as aforestated resulted in bringing down uncommitted inventory levels, Indian leaf tobacco exports were impacted by contraction in global demand, lower domestic crop production and significant currency devaluation in competing origins. Consequently, Indian leaf tobacco exports fell to an eight-year low of 200 million Kgs. thereby adversely impacting the earnings of the tobacco farming community.

Despite such challenging market conditions, the Company reinforced its leadership position as the largest Indian exporter of unmanufactured tobacco with further improvement in market standing. This was achieved through new business development and enhanced value delivery to existing customers by leveraging the Business's expertise in crop development, superior leaf procurement processes and world-class processing facilities. The Business continued to provide strategic sourcing support to the Company's Cigarette Business meeting all requirements at competitive prices.

During 2016-17, world wheat production increased by 16 million tonnes to about 751 million tonnes mainly due to higher production in Australia and Russia. While higher global production led to surplus inventory in the international markets, India had to contend with lower wheat crop availability during the year as the 2015 crop output (marketed in 2016) was adversely impacted due to unfavourable weather conditions. In order to alleviate the shortage of supplies and rising prices in the domestic market, the Food Corporation of India scaled down procurement levels and released higher quantum of wheat from its buffer stocks. In addition, the Government reduced Customs Duty on wheat leading to the import of over five million tonnes from Ukraine and Australia in 2016-17. The Business leveraged its wide geographical sourcing network, multiple sourcing models including imports, to secure supplies of critical grades with benchmark quality towards meeting the growing requirements for Aashirvaad atta. Substantial savings were delivered by the Business through efficient logistics management and other cost-optimisation initiatives. The Business also leveraged its strong network comprising suppliers, millers and customers to supply significant quantities of imported wheat in the domestic market.

The Business also leveraged its extensive sourcing network and associated infrastructure in key growing areas coupled with well entrenched farmer linkages to source high quality fruit pulp for the Company's 'B Natural' brand. The key interventions in this area include strategic plantation development for key fruits, varietal segregation at source for improved colour and taste, customised fruit collection systems for identified fruits, establishing suitable processing protocols and product standardisation.

The Business provided strategic sourcing support to the Branded Packaged Foods Business for the launch of ITC Master Chef range of blended and 'Super Safe' spices. The Company's range of 'Super Safe' spices adhere to stringent EU standards, which require the products to be tested for over 470 pesticide residues as compared to nine under Indian regulations.

Earlier this year the Company forayed into the Premium Frozen Prawns segment under the 'ITC Master Chef' brand. These high quality 'Super Safe' prawns are nurtured and harvested in world-class farms which adhere to extremely stringent international hygiene standards and leverage the Agri Business's experience of over 40 years in exporting prawns to the most demanding markets in the world such as Japan, US, EU etc. The products have received encouraging response in the launch markets and will be progressively rolled out to target markets.

Please refer to the Agri Business section in the Report of the Directors & Management Discussion and Analysis for the financial year ended 31st March 2017 and Media Releases on quarterly results for further details.

Q25. Please provide an update on the Company's Paperboards, Paper and Packaging Segment.

Answer: Paperboards, Paper & Packaging Segment Results registered a robust growth of 18% during the quarter driven by richer product mix, structural cost saving initiatives and benign input costs. Growth in Segment Revenue, however, remained muted on account of subdued demand environment prevailing in the FMCG and legal Cigarette industry, surplus capacity in the domestic industry alongwith zero duty imports under Free Trade Agreement with ASEAN countries and cheap imports from China.

The Company sustained its leadership position in the VAP segment and consolidated its preferred supplier status amongst leading end-use customers and brands. The Business fortified its product portfolio by upgrading select variants and introducing value-added offers such as moisture resistant, grease resistant, medical grade peel-clean paper etc., thereby maintaining its lead over competition. The Specialty Papers portfolio was also expanded with the launch of new grades to service the needs of customers. The Business sustained its leadership position in the sale of eco-labelled products, volumes of which grew by appx. 8% during the year. The Business continues to be a leading quality player in Writing & Printing paper segment, leveraging strong forward linkages with the Company's Education and Stationery Products Business. In the Specialty Papers segment, the Company sustained its leadership position in the pharma leaflets and thin printing segments.

In 2016-17, the Business clocked its highest ever saleable production of appx. seven lakh tonnes - a reflection of its relentless focus on operational excellence and quality. The Business continues to make investments in capacity augmentation, quality and efficiency enhancement, wastage reduction and productivity improvement, benchmarked with international standards.

The Company was recently chosen as the knowledge and implementation partner of National Green Highways Mission under National Highway Authority of India (NHAI), which has been entrusted with the task of planning, implementing and monitoring roadside plantations along one lakh kilometres of national highways. In this regard, the Company signed an agreement with the NHAI to green around 200 hectares of land along NH-44 and NH-40 on a pilot basis.

The Business successfully commissioned a 46 MW wind energy project in Andhra Pradesh in July 2014, which has been generating wind power since then. As reported in previous years, permission for inter-state wheeling of power was not granted by the authorities post bifurcation of the State of Andhra Pradesh. Consequently, the majority of the intended benefits from this large investment did not fructify with only a minor portion of the wind power generated by the project being used by the Company's units in Andhra Pradesh and the balance being sold to the state power grid at nominal rates. After several representations and discussions with the concerned authorities on the matter, the Company received permission during the year for wheeling of power from Andhra Pradesh to Telangana, thereby enabling the Bhadrachalam mill to utilise wind energy to meet its energy requirements. While clearances required for inter-state wheeling of power are now in place, the regulatory framework for levy of charges, banking of power and deviation settlement are still evolving. Consequently, the Company continues to bear charges/levies at multiple points which have adversely impacted the attractiveness of the investment. The Company continues to engage with State and Central regulatory authorities towards seeking relief from such additional levies/charges and remains hopeful of an expeditious resolution of the matter.

Capacity utilisation of India's first Bleached Chemical Thermo Mechanical Pulp mill (BCTMP), recently commissioned by the Business, was progressively ramped up thereby reducing dependence on imported pulp. The Business has also commissioned a 36 MW high pressure energy efficient power plant at the Bhadrachalam unit which will reduce coal consumption and consequently, the Company's carbon footprint.

The integrated nature of the business model comprising access to high-quality fibre from the economic vicinity of the Bhadrachalam mill, in-house pulp mill and state-of-the-art manufacturing facilities along with clear market leadership in value-added paperboards and a robust forward linkage with the Education and Stationery Products Business strategically positions the Company to further consolidate and enhance its leadership status in the Indian Paperboard and Paper industry.

The Company's Packaging and Printing Business is a leading provider of superior value-added packaging for the consumer packaged goods industry. The Business also provides strategic support to the Company's FMCG Businesses by facilitating faster turnaround for new launches, design changes, ensuring security of supplies and delivering benchmarked international quality at competitive cost. The Business caters to the packaging requirements of leading players across several industry segments viz., Food & Beverage, Personal Care, Home care, Apparel, Consumer Electronics, Pharma, Liquor and Tobacco. With its comprehensive capability-set across multiple platforms, coupled with in-house cylinder making and blown film manufacturing lines, the Business continues to provide innovative solutions to several key customers in India and overseas.

In line with its strategy of consolidating its position as a 'one-stop shop for packaging solutions', during the year the Business invested in new product lines viz., rigid boxes and flexo corrugated packaging, and augmented capacity in the carton and flexibles packaging segments with the addition of state-of-the-art lines at its facility at Tiruvottiyur. With world-class technology across a diverse range of packaging platforms, best-in-class quality management systems and a distributed manufacturing footprint, the Business is well positioned to rapidly grow its external business while continuing to service the requirements of the Company's FMCG Businesses.

Please refer to the Paperboards, Paper & Packaging section in the Report of the Directors & Management Discussion and Analysis for the financial year ended 31st March 2017 and Media Releases on quarterly results for further details.

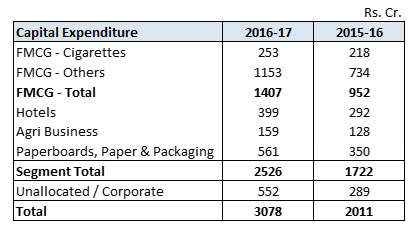

Q26. Please provide details of the Company's Capital expenditure by Business.

Answer: The Company's Capex during the last two financial years is tabulated below:

Q27. Please provide an overview of the capex plan of the Company.

Answer: The Company's capex plans are directed primarily towards capacity gearing, productivity enhancement, ensuring the highest standards in quality and environment, health & safety, and R&D.

One of the key elements of the capex plan going forward is to invest in setting up state-of-the-art owned integrated consumer goods manufacturing and logistics facilities across regions in line with long-term demand forecasts. Currently, over 20 projects are underway and in various stages of development - from land acquisition/site development to construction of buildings and other infrastructure.

In the Hotels Business, the Company is progressing the construction of new hotels in Kolkata, Hyderabad and Ahmedabad. Besides, WelcomHotels Lanka Private Ltd. - a wholly-owned subsidiary of the Company - made good progress towards setting up a luxury hotel christened 'ITC One' and a super-premium residential apartment complex , 'Colombo One - Private Residences' at a strategic location in Colombo.

The major items of capital expenditure in the Paperboards, Paper and Packaging segment going forward comprise paperboards & specialty paper capacity augmentation/machine rebuild at the Bhadrachalam and Tribeni units and capacity augmentation in Cartons and Flexibles packaging at the Tiruvottiyur unit.

Overall, the Company estimates capex of around Rs. 20000 crores over the next 5 years (excluding investments for inorganic growth and acquisition of trademarks, other intellectual property, etc.). However, this would depend on several factors such as pick-up in economic activity and improvement in demand conditions, timely acquisition of land at desirable locations, obtaining approvals from the concerned authorities in a timely manner etc.

Q28. Why has the Segment Capital Employed increased by Rs. 217 crores from Rs. 22385 crores as at 30th September 2016 to Rs. 22602 crores as at 30th September 2017?

Answer: The increase in Segment Capital Employed was primarily on account of higher Net Fixed Assets (net of depreciation) towards capacity augmentation in FMCG businesses, ongoing investments in Hotels, and cost reduction related investments in Paperboards, Paper and Packaging business partly offset by incremental GST liability.

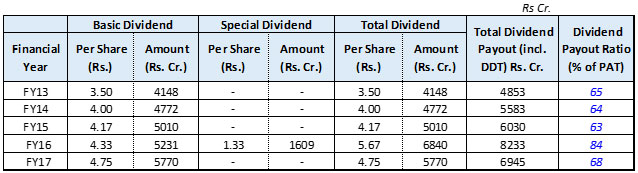

Q29. What are the dividend payout trends in recent years? What is the Dividend policy of the Company?

Answer: Dividend paid out by the Company for the last 5 years is given below:

Please refer to the following link for the Dividend Distribution policy of the Company.

http://www.itcportal.com/about-itc/policies/dividend-distribution-policy.pdf

Q30. Please explain the Company's 'Triple Bottom Line' philosophy.

Answer: Inspired by the opportunity to sub-serve larger national priorities, the Company redefined its Vision to not only reposition the organisation for extreme competitiveness but also make societal value creation the bedrock of its corporate strategy. This super-ordinate Vision spurred innovative strategies to address some of the most challenging societal issues including widespread poverty, unemployment and environmental degradation. The Company's sustainability strategy aims at creating significant value for the nation through superior 'Triple Bottom Line' performance that builds and enriches the country's economic, environmental and social capital. The sustainability strategy is premised on the belief that the transformational capacity of business can be very effectively leveraged to create significant societal value through a spirit of innovation and enterprise.

The Company is today a global exemplar in sustainability. The Company's models of sustainable development have led to the creation of sustainable livelihoods for around six million people, many of whom belong to the marginalised sections of society. The Company has also sustained its position of being the only Company in the world of comparable dimensions to have achieved the global environmental distinction of being carbon positive (for 12 consecutive years), water positive (for 15 years in a row) and solid waste recycling positive (for 10 years in succession).

The Company's strategy of adopting a low-carbon growth path is manifest in its growing renewable energy portfolio, establishment of green buildings, large-scale afforestation programme, achievement of international benchmarks in energy and water consumption. Today, over 48% of the Company total energy requirements are met from renewable energy sources - an outstanding performance given its large manufacturing base. Further, premium luxury hotels, several office complexes and factories of the Company are certified at the highest level by the US Green Building Council / Indian Green Building Council and the Bureau of Energy Efficiency (BEE).

The Company's 14th Sustainability Report, published during the year detailed the progress made across all dimensions of the 'Triple Bottom Line' for the year 2016-17. This report is in conformance with the latest Global Reporting Initiative (GRI) Guidelines - G4 under "In Accordance - Comprehensive" category and is third-party assured at the highest criteria of "reasonable assurance" as per International Standard on Assurance Engagements (ISAE) 3000.

Please refer to the following link http://www.itcportal.com/sustainability/sustainability-report-2017/sustainability-report-2017.pdf for Sustainability Report 2017.

In addition, the Business Responsibility Report (BRR), annexed to the Report and Accounts 2017, maps the sustainability performance of the Company against the reporting framework suggested by Securities and Exchange Board of India.

Q31. Please provide an update of the Company's Corporate Social Responsibility Programme.

Answer: The Company's Corporate Social Responsibility (CSR) programme aims to address the challenges arising out of poverty, environmental degradation and climate change through a range of activities with the overarching objective of creating sustainable sources of livelihood for stakeholders many of whom represent the poorest in rural India.

The footprint of the Company's CSR programme can be viewed at a glance in the following chart:

| Intervention Areas | Unit of Measurement | Cumulative till date |

|---|---|---|

| Social and Farm Forestry Soil and Moisture Conservation Programme |

Lakh Acres Lakh Acres |

6.62 8.36 |

| Sustainable Agricultural Practices Compost Units |

Number |

36,027 |

| Sustainable Livelihoods Initiative Cattle Development Centres Animal Husbandry Services |

Number Artificial Inseminations (in lakhs) |

228 21.03 |

| Economic Empowerment of Women Ultra Poor Women covered Self Help Group Members Livelihoods created |

Number Number Number |

13,800 36,100 54,732 |

| Primary Education Children covered |

Number (in lakhs) |

5.48 |

| Health and Sanitation Low Cost Sanitary Units Households covered under Solid Waste Management |

Number Number |

27,770 65,577 |

| Vocational Training Students Enrolled |

Number |

49,639 |